Ratepayers Finance Exorbitant Utility Profits

As electric bills soar, executive pay steadily climbs

March 25, 2026

Share

It has been more than three years since the Rhode Island Public Utilities Commission unanimously signed off on a historic 47% rate hike that increased an average household’s monthly electric bill by nearly $51.

The corporate-friendly commissioners told low-wealth families and advocates from the George Wiley Center, the Poor People’s Campaign, Sisters of Mercy, and the Rhode Island Interfaith Coalition to Reduce Poverty they were limited in their powers to reject the hike. They said Rhode Island Energy, which had just bought National Grid, had acted properly when formulating the historically high rate increase.

Rhode Island Energy is a subsidiary of the Pennsylvania Power and Light Corp., which reported $1.18 billion in earnings last year. In 2024, the compensation package for the parent company’s CEO, Vincent Sorgi, was worth $11,355,743. In 2023, the first full year after the PPL Corp. acquired National Grid, Sorgi’s compensation package was worth $11,969,556.

The median household income in Rhode Island is $86,372, or 131 to 139 times less than Sorgi’s pay.

The state’s median household income is also considerably less than what the three members of the R.I. PUC are paid. Last year, PUC chair Ronald Gerwatowski was paid $158,477, 50% higher than the average and 48% higher than the median salary for public utilities commissioners. Member Abigail Anthony was paid $140,615, 33% and 31% higher. Member Karen Bradbury was paid $110,971, 5% and 3% higher.

The average Rhode Island utility bill for a home that uses 500 kilowatt-hours of electricity a month now exceeds $150. In 2021, prior to the infamous rate hike, the average bill for the same usage was about $110. In 2017, it was about $100 a month.

The result of continued rate hikes and Sorgi’s relentless feeding at the trough? Twenty-seven percent of Rhode Island electric customers are delinquent on their bills. More than half of those delinquent customers, some 69,000 electric accounts, are more than 90 days behind.

Low-income residents aren’t alone in struggling to pay their electric bills. The only people not stuck in this always-tightening electric vice are the wealthy, such as Sorgi, who has an estimated net worth of at least $27.2 million.

As electric bills escalate, the pay of utility executives steadily climbs. It’s not a coincidence.

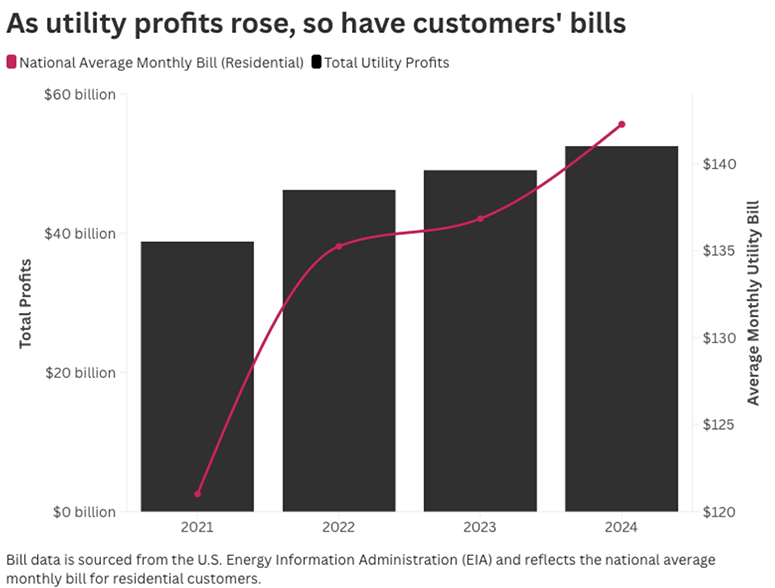

Profit margins of investor-owned utilities, such as Rhode Island Energy and Eversource, increased last year, according to an analysis by the Energy and Policy Institute, a nonprofit watchdog “that exposes the harms posed by fossil-fuel and monopoly utility interests to ratepayers, democracy, and the climate.”

Investor-owned utilities kept as profit an average of 14.6 cents of every dollar they collected from customers in 2025, up from 12.8 cents from 2021 to 2024, according to the analysis. For a customer paying a $200 monthly electric bill, that means about $30 went to corporate profits.

Investor-owned utilities typically operate as regulated monopolies within defined service territories, where customers can’t choose another provider and state regulators, it turns out, basically rubber-stamp the rates utilities request. The rates are designed to cover the costs of operating the electric system and to provide utilities with a return on investment for shareholders.

Despite its central role in the utility business model, the share of electricity revenue that utilities retain as profit is rarely analyzed, according to the Energy and Policy Institute (EPI).

EPI’s recent analysis found investor-owned utilities earn significantly more than the allowed returns on equity set by regulators. But nobody holds them accountable, because, to paraphrase the R.I. PUC, there’s not much regulators can do. There is. They just don’t.

A recent analysis by the American Economic Liberties Project estimated that excess return on equity (ROE) costs customers some $50 billion annually, or about $300 per household. That is money ratepayers are paying not for electricity, not for infrastructure, but for profits that exceed what investors need to be fairly compensated for providing capital.

It’s a scam.

In 2024, the average authorized ROE for regulated U.S. utilities was 9.7%, while the average of 34 major investment firms’ long-term equity return forecasts for the broad U.S. market was 6.7%, the EPI analysis noted.

Even the highest individual forecast, 8.3%, was lower than the average authorized utility return on equity. That gap is particularly striking because utilities, with their regulated monopoly status and predictable earnings, are lower-risk investments than the market as a whole; their cost of equity should be below the market average, not above it, according to EPI.

To illustrate how excess earnings impact ratepayers, EPI used the building of a new $1 billion power plant financed with equal shares of debt and equity — using an example 10% ROE and 5% debt rate over 30 years. Customers would pay about $775 million in profits to shareholders alone, on top of the full $1 billion in capital recovery. Add in debt interest, and total customer payments for that single asset approach $2.2 billion — a $1 billion investment, paid for more than twice over.

EPI reviewed public financial reports from 110 investor-owned electric utilities between 2021 and 2024. Seventy-nine of those utilities provided financial data for 2025 in time to be included in the report, which tallied more than $200 billion in net income over the five-year period.

Utility executives and shareholders are making a killing as an increasing number of U.S. households struggle to pay ever-escalating electric bills. Renewable energy isn’t the reason our electricity bills are so high.

Frank Carini can be reached at [email protected]. His opinions don’t reflect those of ecoRI News.

No more investing in any fossil fuel infrastructure. Time to go 100% clean power becasue the price of gas factorsdinto all of this and where a utility uses more gas, the people pay more.

executive salaries are excessive compared to the bulk of the population in utilities, and almost all other industries too, and its getting worse. And I understand the political appeal of castigating the utilities that we pay to get power. But it should also be noted in the last 2 winters electric rates declined slightly, so “electric rates escalate” is somewhat misleading. Further, I think the problem isn’t so much the utilities as it is our reliance on natural gas instead of renewables. In winter we use a lot of gas for both heating and electric generation, and a lot of LNG is shipped to Europe to replace sanctioned Russian supplies – (indeed I think one reason for our Ukraine war involvement is to get the European energy market away from Russia) I think we should prioritize a common interest with the utilities in developing renewables, especially off-shore wind, which is much needed if we are to electrify heating and r-transportation without fossil fuels, and they benefit by buying air and wind as fuel to transmit instead of fossil fuels with volatile and truly escalating prices

Our usage charge and delivery charge our identical. So our bills are double what

they should be. Is there any rebate possible for the past overcharges of the last

two years?